Rethinking Capital Gains Tax on Land and Housing

Introduction

Decreasing housing affordability and increasing wealth inequality in Australia have renewed debate about the Capital Gains Tax (CGT) and the associated 50% discount.

The current debate appears to conflate two distinct issues: adjusting gains for inflation, which is the primary objective of the discount, and determining how much of the real gain should be retained by the investor.

These are separate concerns and should be treated as such, particularly for assets where gains are primarily derived from owning and trading rights to residential land and housing (land and housing).

This article proposes treating inflation adjustment and real gain distribution as two distinct processes and shows how a separate progressive tax schedule could be applied to gains from land and housing.

Background

When an individual or trust sells an asset such as land and housing, there can be a financial gain. The gain is the difference between the amount they paid for the asset and the amount they sell it for. The gain is included in taxable income and taxed at the applicable marginal income tax rate.

A long-standing principle is that only the real gain, that is the gain adjusted for inflation, should be taxed. This principle is reasonable.

Prior to 1999, gains from investments that were held for over 12 months were indexed to inflation using a formula that was generally regarded as complex. The indexation method was replaced with a flat 50% discount, intended as a simplified approximation of inflation.

The inflation-adjusted gain, the real gain, is then taxed at the individual’s or trust’s marginal income tax rate for the year in which the gain occurs. This means large one-off gains are taxed as though they are recurring annual income. The marginal rate that is applied depends on total income in that particular year.

It has long been argued that the switch to the discount methodology has contributed to rising asset values and increasing wealth inequality.

There is some weight to that argument based on:

Investors typically price assets based on expected after-tax returns. If a tax falls, the maximum price investors are willing to pay theoretically rises. If the discount over-compensates for inflation, and it likely does in most periods, the excess becomes a structural tax benefit. That benefit is capitalised into higher purchase prices, contributing directly to upward pressure on land and house prices.

The discount methodology is simpler and more transparent than indexation. When tax outcomes are easier to model, more individuals and trusts can confidently participate in land and housing investment.

The shift from indexation to the flat discount coincided with a period of strong credit growth and rising asset values. While not the sole cause, the simplified and potentially more generous treatment likely amplified that upswing by increasing expected after-tax returns at a critical point in the cycle.

Land and housing are already central drivers of wealth inequality. When policy settings increase after-tax returns for investors, it can concentrate wealth with existing asset holders. The effect compounds over time as gains are reinvested and capitalised into further asset acquisition.

The current conversation: adjust the discount

The current conversation is centred on adjusting the discount to improve housing affordability and reduce wealth inequality. This approach conflates two distinct policy questions that should ideally be examined independently.

What is the appropriate discount to be applied as an approximate for inflation?

How much of the real gain should the investor retain?

Let’s break these two issues down.

The first question is largely technical. If a 25% discount more accurately reflects average inflation than the 50% discount, then the discount could be reduced to 25%. If another percentage more closely reflects actual inflation, for example 33%, then that percentage could be adopted instead.

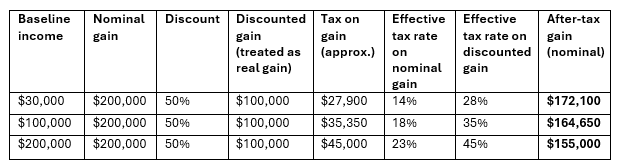

The table below shows how a $200k nominal gain and the 50% discount is applied to three different baseline incomes and the nominal amount that is retained by the investor.

Table 1: Three incomes with $200k gain and 50% discount

*Based on 2025–26 marginal tax rates for individuals, excluding Medicare levy and other adjustments.

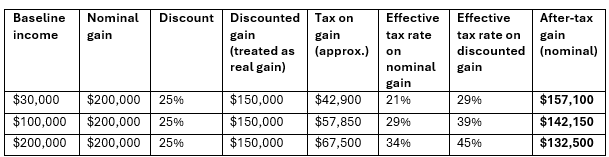

The table below shows when a 25% discount is applied, the effective tax rate on the nominal gain is closer to the marginal income tax rates for those three baseline incomes. It also shows the after-tax nominal amount that is retained by the investor is relatively close to the amount that is retained when a 50% discount is applied (Table 1).

Table 2: Three incomes with $200k gain and 25% discount

*Based on 2025–26 marginal tax rates for individuals, excluding Medicare levy and other adjustments.

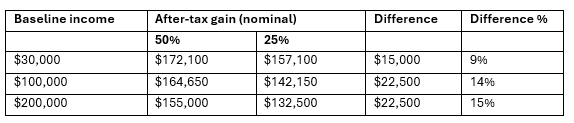

Table 3 below suggests that reducing the discount alone does not materially reduce after-tax nominal gains.

Table 3: Comparison between 50% discount and 25% discount

It is difficult to see how an alternative discount that produces only a modest change in after-tax gains would materially alter investment behaviour or significantly affect wealth inequality.

The second question of how much of the real gain should be taxed is not a technical matter. It is a political and ethical choice about housing affordability, wealth distribution and economic growth.

As a reminder, the current policy, excluding the accuracy of the 50% discount, is for the investor to keep 100% of the after-tax gain.

This position is challengeable on the following grounds:

It encourages investment in rights to land and housing, which claims existing wealth from others, rather than investment that improves productivity and national income. In summary, it encourages wealth transfer, not wealth creation.

Applying the real gain to the marginal income tax rate in the year it is realised encourages deferral of gain realisation. Investors are incentivised to hold assets longer and crystallise gains in years when their other income is lower, most commonly in retirement. This encourages asset accumulation and concentration rather than broader distribution.

Compared with many productive business investments, long-term residential landholding often involves lower operational risk while still generating substantial gains. Ideally, expected returns should broadly reflect the level of risk relative to other asset classes and their market structures.

A substantial portion of gains from land and housing reflects increases in underlying land values, which are driven by population growth, infrastructure investment, credit expansion and broader economic development. These drivers are largely societal rather than the result of individual effort. The private capture of these gains therefore raises legitimate distributional questions. In summary, the current position incentivises accumulation of unearned rather than earned gains.

An alternative approach

In considering how much of the real gain should be returned to society and how much should be retained by the investor; several guiding principles may be relevant:

Tax policy should avoid disproportionately rewarding wealth transfer over wealth creation.

Investment incentives should favour investment that enhances productivity and wealth creation.

Expected returns should broadly reflect risk.

Where gains arise primarily from societal development rather than individual effort, a significant portion should be returned to the broader community.

In applying these principles, it’s clear that an alternative and more progressive tax methodology for capital gains received from land and housing should be considered.

Perhaps one way to pursue these principles would be to introduce a separate tax schedule for gains derived from land and housing, where the marginal tax rate increases with the size of the gain. Put simply, the larger the gain, the higher the marginal tax rate that would be applied to that gain.

To avoid concerns about double taxation, this tax schedule could operate as a final tax. Once calculated, the after-tax gain would not be added to other income for that year. The after-tax gain is what the individual or trust retains.

Put together, the process would be:

Apply the accurate inflation adjustment (discount) to the nominal gain to derive the real (taxable) gain.

Apply the progressive tax schedule to the real (taxable) gain to determine the tax obligation and the after-tax gain for the investor.

This structure would reduce incentives for income smoothing, while recognising gains from land and housing as a distinct category of income. This structure could, in principle, also provide a framework for reconsidering the tax treatment of owner-occupied housing, should future policy debate move in that direction.

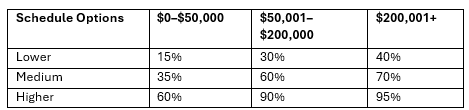

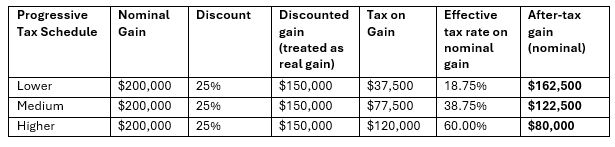

Tables 4 and 5 below show how a $200k nominal capital gain and a 25% discount, assuming this is a more accurate approximation of inflation, is used to calculate a discounted gain that is then taxed under three progressive options.

Table 4: Example progressive tax schedule

*Even under a highly progressive schedule, investors would retain a share of large gains.

Table 5 shows the lower option generates a nominal after-tax gain that is similar to the gains that are retained with the current approach. The medium and higher gains reduce the after-tax gain to levels that are more consistent with the principles outlined above.

Table 5: Application of 25% discount and example progressive tax schedule

The approach demonstrates that materially different distributional outcomes are possible, irrespective of the inflation adjustment.

It’s worth noting that a progressive tax schedule by gain size may still create incentives to stagger disposals across years; careful design (e.g. anti‑avoidance rules, aggregation of related disposals) would be needed to limit this.

Conclusion

Current policy settings generate substantial after-tax gains for investors and contribute to increasing wealth concentration and sub-optimal economic allocation.

Adjusting the discount alone is unlikely to materially change housing affordability or wealth inequality.

By separating the inflation adjustment and the distribution of gains, greater understanding can be reached about the outcomes that could be achieved through reform.

By taxing the real gain progressively and separately from income, the gains from land and housing, which largely arise from societal factors rather than individual effort, could be redistributed to the broader community.

Any reform would require clear definitions, careful design, transition arrangements and coordination with states and territories to avoid unintended behavioural distortions.

Importantly, any reforms to CGT on land and housing should be coordinated with strengthened, broad‑based land taxes at the state and territory level, consistent with previous national tax reviews, and implemented with appropriate transition arrangements.